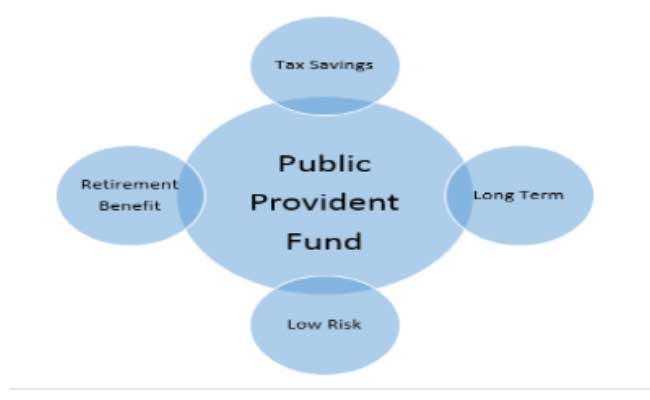

Public Provident Fund: An Investment for Your Future

Public Provident Fund (PPF) is a popular long-term investment option offered by the Government of India to its citizens. It was introduced in 1968 with the objective of encouraging savings and providing a retirement corpus for individuals. The scheme is managed by the National Savings Institute (NSI) and is available across all authorized banks and post offices in India. In this article, we will discuss the features, benefits, and limitations of the PPF scheme.

Features of Public Provident Fund

The PPF scheme is open to all Indian citizens, whether employed or self-employed. A minimum investment of Rs. 500 per year is required to open a PPF account, and the maximum limit for the same is Rs. 1.5 lakh per year. The account can be opened with any authorized bank or post office and can be operated for a period of 15 years. It can be extended in blocks of 5 years after the completion of the initial 15-year term.

The interest rate for the PPF scheme is decided by the Government of India and is revised every quarter. As of April 2023, the interest rate is 7.1% per annum, which is compounded annually. The interest earned on the PPF account is tax-free, and the contributions made towards the scheme are eligible for tax benefits under Section 80C of the Income Tax Act.

One of the unique features of the PPF scheme is that it allows partial withdrawals after the completion of the 6th year. The maximum amount that can be withdrawn is 50% of the balance at the end of the 4th year or the immediately preceding year, whichever is lower. The withdrawals can be made once every year, and the account holder can choose the amount and the timing of the withdrawal. However, if the withdrawal is made before the completion of 5 years, the account will be deemed closed, and the entire amount will be refunded to the account holder after deducting a penalty of 1%.

Benefits of Public Provident Fund

The PPF scheme offers several benefits to the account holder, which makes it an attractive investment option. Some of these benefits are as follows:

- Tax benefits: The contributions made towards the PPF account are eligible for tax benefits under Section 80C of the Income Tax Act. The interest earned on the account is also tax-free, which makes it a tax-efficient investment option.

- Long-term investment: The PPF scheme has a tenure of 15 years, which makes it a long-term investment option. It is ideal for individuals who are looking to save for their retirement or other long-term goals.

- Guaranteed returns: The interest rate for the PPF scheme is decided by the Government of India and is guaranteed for the entire tenure of the account. This ensures that the account holder earns a fixed rate of return on their investment.

- Flexibility: The PPF scheme allows partial withdrawals after the completion of the 6th year. This provides flexibility to the account holder to withdraw funds in case of an emergency.

- Low risk: The PPF scheme is backed by the Government of India, which makes it a low-risk investment option. The investment is secure and offers guaranteed returns, which makes it an ideal investment option for risk-averse individuals.

Limitations of Public Provident Fund

While the PPF scheme offers several benefits, there are some limitations that need to be considered before investing in it. Some of these limitations are as follows:

- Long lock-in period: The PPF scheme has a lock-in period of 15 years, which makes it unsuitable for individuals who require liquidity in the short term.

![]()

One thought on “Public Provident Fund”