Managing personal finances is an essential part of achieving financial stability. One of the most important factors lenders consider before approving a loan or credit card is the Debt to Income Ratio (DTI). Understanding this financial metric can help you improve your creditworthiness, qualify for better loan terms, and maintain a healthy financial future.

What Is Debt-to-Income Ratio?

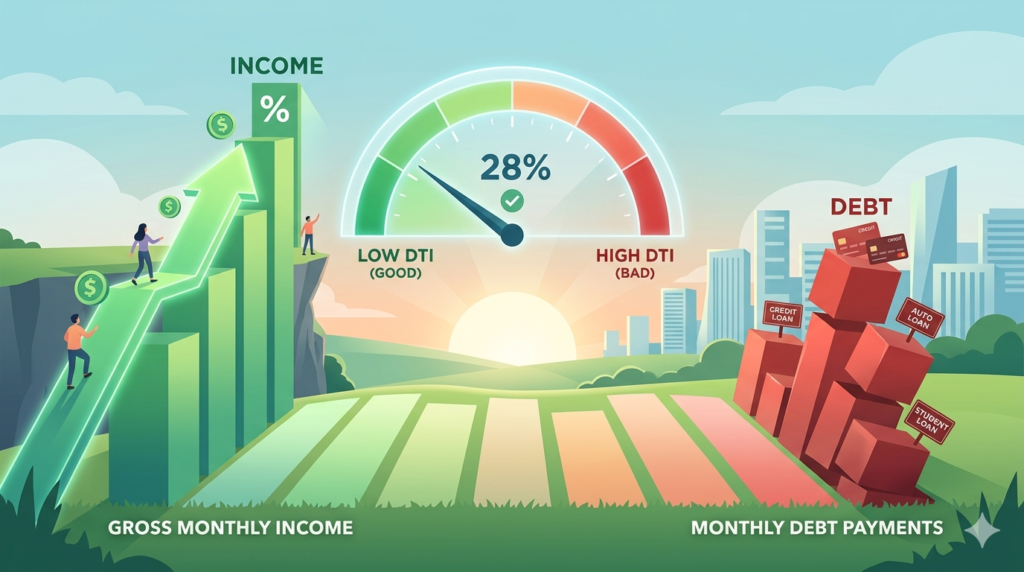

Debt to Income Ratio is a percentage that compares your monthly debt payments to your gross monthly income. In simple terms, it shows how much of your income goes toward paying debts every month.

Lenders use this ratio to determine whether you can responsibly manage additional debt. A lower DTI ratio indicates better financial health, while a higher ratio may suggest financial stress.

DTI Formula

DTI Ratio=Gross Monthly IncomeTotal Monthly Debt Payments×100

For example, if your total monthly debt payments are ₹20,000 and your monthly income is ₹80,000, your DTI ratio would be 25%.

Why Debt-to-Income Ratio Matters

Your debt-to-income ratio plays a major role in financial decisions made by banks and lenders. Whether you are applying for a home loan, personal loan, or car loan, lenders review your DTI ratio to assess risk.

Key Reasons DTI Ratio Is Important

- Helps lenders evaluate repayment ability

- Affects loan approval chances

- Influences interest rates

- Determines borrowing limits

- Reflects overall financial stability

A low DTI ratio can improve your chances of getting approved for loans with favorable interest rates.

Types of Debt-to-Income Ratio

There are generally two types of DTI ratios lenders analyze.

1. Front-End Ratio

This ratio focuses on housing-related expenses, including:

- Home loan EMI

- Property taxes

- Home insurance

It measures how much income goes toward housing costs.

2. Back-End Ratio

This includes all monthly debt obligations, such as:

- Credit card payments

- Personal loans

- Car loans

- Student loans

- Housing expenses

Most lenders pay closer attention to the back-end ratio because it provides a complete picture of your financial obligations.

What Is Considered a Good Debt-to-Income Ratio?

A good DTI ratio depends on the lender and type of loan, but the following guidelines are commonly used:

| Debt-to-Income Ratio | Financial Condition |

|---|---|

| Below 20% | Excellent |

| 20% – 35% | Good |

| 36% – 49% | Average |

| 50% and above | Risky |

Generally, lenders prefer borrowers with a DTI ratio below 36%.

How to Calculate Your DTI

Calculating your DTI ratio is simple. Follow these steps:

Step 1-Add Your Monthly Debt Payments

Include:

- Loan EMIs

- Credit card minimum payments

- Mortgage payments

- Other recurring debts

Step 2-Determine Your Gross Monthly Income

This includes:

- Salary

- Business income

- Rental income

- Bonuses or commissions

Step 3-Divide Debt by Income

Use the DTI formula to find the percentage.

For example:

- Total monthly debt = ₹30,000

- Gross monthly income = ₹1,00,000

Your DTI ratio would be 30%.

How to Improve Your Debt-to-Income Ratio

If your DTI ratio is high, there are several effective ways to improve it.

Pay Off Existing Debts

Reducing outstanding loans and credit card balances lowers your monthly obligations and improves your ratio.

Increase Your Income

You can improve your DTI ratio by:

- Taking freelance work

- Starting a side business

- Requesting a salary increase

Higher income reduces the percentage of debt compared to earnings.

Avoid Taking New Loans

Applying for new loans increases monthly debt payments and can negatively affect your DTI ratio.

Refinance High-Interest Loans

Refinancing can lower monthly EMIs and make debt management easier.

Debt-to-Income Ratio vs Credit Score

Many people confuse DTI ratio with credit score, but they are different.

- Credit score measures your credit history and repayment behavior.

- Debt-to-income ratio measures your ability to handle monthly debt payments.

Both factors are important when applying for loans.

Understanding your debt-to-income ratio is essential for maintaining financial stability and improving your borrowing potential. A healthy DTI ratio not only increases your chances of loan approval but also helps you manage money more effectively.

Freelancerson.com a Free Marketplace for Freelancers and Clients

Read Also: Job Seeker Website Portal

![]()